Title: SW Weekly: Separating The Winners From The Casualties In Hydrogen

From 2019 multi-bagger profits to the brutal 2025 bankruptcies looking past the media narratives to find the technology plays positioned to run next.

I have been following the Hydrogen industry for many years, and I made great initial profits from companies like AFC Energy and Plug Power in 2019. This chart shows the huge win in AFC in 2019/2020 followed by an even bigger loss in 2021.

(AFC energy, Green in Red out )

It was this roller-coaster ride that led me to adopt the Gartner Hype Cycle as a fundamental pillar of my trading plan.

Today, we need to take a fresh look at the hydrogen sector. Share prices across several key players have shown explosive moves higher recently: Plug is up 45% this year, Ballard has climbed 72%, and FuelCell Energy has surged an incredible 228%. I have covered all of these names individually before, but today I want to focus on the broader macro picture: the hydrogen value chain, the hidden physical bottlenecks, and the structural progress being made.

But first, as always, let’s review our performance.

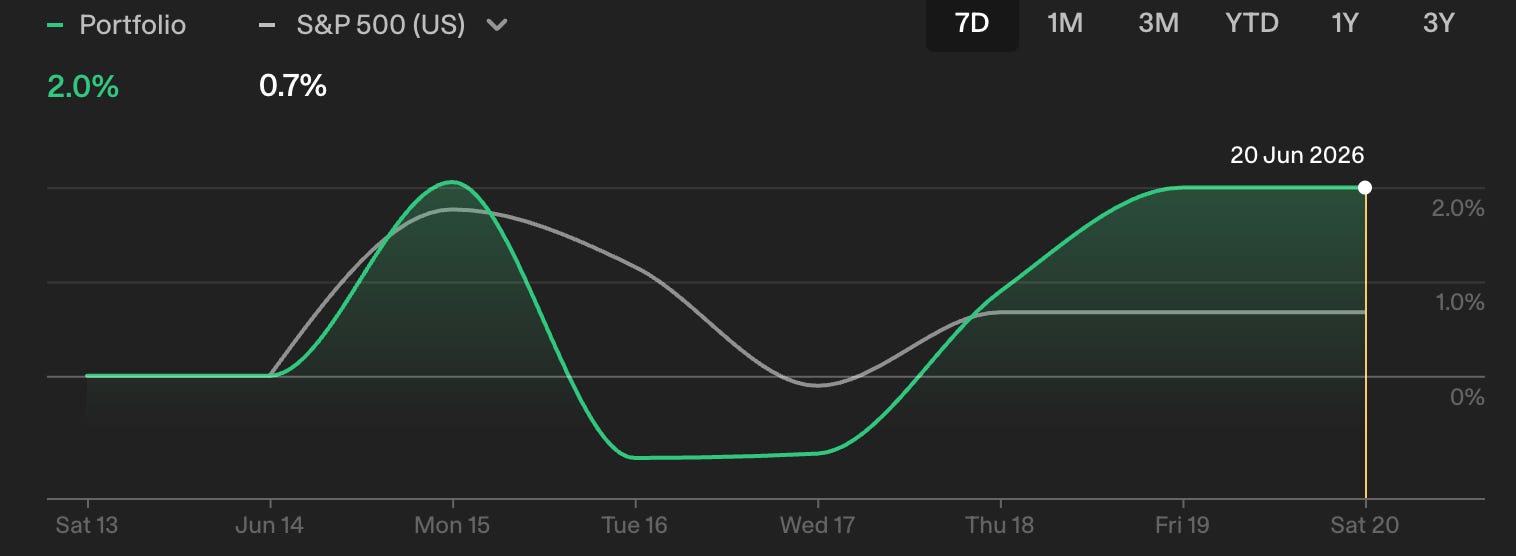

Portfolio Results

SW Trade (short term)

A small rebound this week, but the geopolitical moves surrounding the Iran war caused significant volatility again this week.

SW Trade, the short-term portfolio, beat the S&P, delivering a 2% return this week, but did not recover last week’s losses. Our recent setups are going well—the last 15 trades are averaging a 14% return. However, overall performance is being dragged down by a few legacy positions in robotaxis and recycling stocks. I am sticking to my guns here because the core thesis remains valid, but waiting for emerging tech to fulfill its structural potential can be a test of patience.

SW Trade Chart

Holding through these dry spells is tough, but history shows it’s often the right move. Case in point: my oldest position in nuclear energy was sitting at a painful -53% earlier this year. I opened it in May 2025. In the last 30 days, it surged 39%, bringing us right back to the edge of break-even.

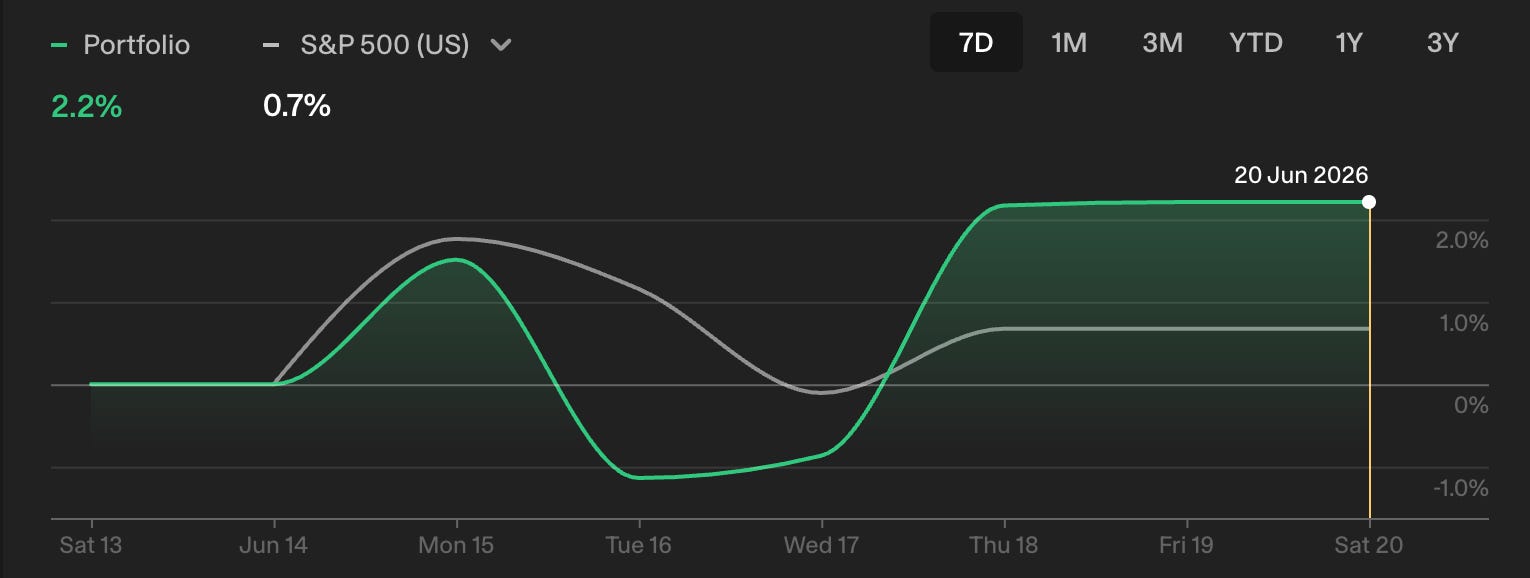

SW Invest (long term)

SW Invest, my longer-term portfolio, continues to outperform. It is still very early days for this portfolio as we are only in month two. We have now made 7 investments, and 6 of them are profitable.

I did not make any new trades or investments last week and did not close any positions.

The Hydrogen Sector

Are the massive share price moves we are seeing a true reflection of a structural shift in the industry, or is it just retail investors falling for the same old company press releases? Before I risk capital here, I want some proof that the sector is moving toward self-sustaining, profit-generating operations.

The Hype Cycle

Gartner plots a technology’s market expectations against the reality of what it can actually achieve. Though they focus on corporate adoption, the same pattern plays out in the stock prices of the pure-play tech small-caps I follow.

In December 2023, I wrote this article on Ballard Power

It was my view that Ballard had been through the peak of expectations and was now firmly in the trough of disillusionment, since then the stock has increased 15% in value, a poor return when the S&P is up 60%. Because I didn’t give the stock a “strong buy” rating, it never made it into the portfolio (which was at the time called the Strong Buy portfolio)

If Ballard and its peers are transitioning to the Slope of Enlightenment, it becomes a definitive Strong Buy.

The Slope of Enlightenment is my target zone. It’s the phase where companies stop surviving on non-binding letters of intent (LOIs), vague joint ventures, and pilot testing, and start booking real, commercial, profit-oriented contracts.

The early signs of a commercial shift are growing:

Ballard Power has secured a single commercial order for 500 bus engines, and its rail engine vertical scaled from just $0.1 million in 2024 to $5.1 million in 2025.

Upstream Infrastructure: Massive, industrial-scale electrolyzers are being deployed globally, and pure-play stock prices are finally reflecting it.

If the sector is truly moving up this slope, it will become a gold mine for investors who position themselves early in the right alpha targets.

Understanding Hydrogen

The hype bubble of 2020 was built on the fallacy that hydrogen would power passenger cars, consumer electronics, and home heating, and even more ridiculously that it would do it soon. The problem of energy efficiency was ignored, along with the problems of running a hydrogen economy.

The issue boils down to energy efficiency. Producing, compressing, and converting hydrogen loses energy at every single step. In a hydrogen fuel cell car, only about 30% of the original electricity generated reaches the wheels. A battery electric car delivers closer to 90% efficiency. For consumer cars, batteries won the war long ago.

However, outside of the US, aggressive environmental mandates and energy security concerns are forcing a shift. For nations without native oil and gas assets, hydrogen offers a path to energy independence. More importantly, there are two massive, heavily polluting global sectors where batteries physically cannot do the job: Steel and Heavy Transport.

Steel Production

Steel production accounts for around 8% of global emissions. In traditional steel making, iron ore is mixed with coke/coal and heated in massive blast furnaces. The reaction strips oxygen from iron and produces large amounts of carbon dioxide. The Chemical formula is

In hydrogen metallurgy, the use of coal/coke is replaced by hydrogen. The chemical reaction is.

With only water being released instead of carbon dioxide.

Heavy-duty Transport

To power a long-haul Class 8 semi-truck with batteries, you would need a battery pack weighing roughly 6 tons, and you’d have to stop and charge it every couple of hundred miles. In deep-sea marine environments and aviation, batteries are physically impossible—the weight penalty prevents planes from taking off, and there is no charging grid in the middle of the Atlantic.

Hydrogen has three times the energy density of gasoline by weight. By combining a lightweight fuel cell with high-pressure carbon-fiber storage tanks, you get a zero-emission heavy transport vehicle that refuels in minutes. If you want to double your range, you simply build a larger storage tank.

The Hydrogen Value Chain

The hydrogen value chain looks straightforward: you make it (Production), you move it (Logistics), and you use it (Conversion via Fuel Cells).

The problem is in step 2. Hydrogen is a nightmare substance to transport over any distance.

Hydrogen Production

At the moment, there are three ways to produce Hydrogen

Steam methane reforming, accounting for 95% of all hydrogen produced, involves mixing natural gas CH4 with high-temperature water H2O, which produces hydrogen and lots of CO2. It is a low-cost process, and the hydrogen produced is known as grey hydrogen unless it is produced with carbon capture, in which case it is known as blue hydrogen. (Brown hydrogen uses coal instead of natural gas)

Methane Pyrolysis. This is an emerging alternative, instead of using steam the process uses plasma at extreme heat to blast the natural gas apart. No oxygen is introduced to the system so the hydrogen leaves behind carbon black rather than carbon dioxide which has secondary uses in tires and plastics.

Electrolysis: This involves splitting water, H2O, the only by-product is oxygen released into the atmosphere, and if renewable energy is used, it is known as green hydrogen. The technology to split water can be Proton Exchange Membranes or alkaline electrolyzers.

Downstream Logistics

If production is adjacent to the use case, perhaps a steel mill or factory then the hydrogen can be piped directly.

However, moving hydrogen over longer distances is an insurmountable problem.

Hydrogen is the smallest and lightest element in the universe- physics and geometry explain why you can not transport it economically.

To ship pure hydrogen, you must liquify it by chilling it to -253 °C. Maintaining that extreme temperature across the oceans consumes nearly half of the hydrogen’s energy. Even in top-tier cryogenic hulls, you lose roughly 1% of your cargo every single day due to boil-off. On an 18-day voyage, you use more energy than contained in the delivered hydrogen..

You can’t truck it either. Because it is so light, you need to compress it to 700 bar or freeze it again to -253 °C. If you had a 40-tonne truck, 39 tonnes would be taken up by the incredibly thick storage tubes needed to cope with the pressure or the temperature.

You can’t pipe it through existing pipelines. The hydrogen molecule is so small it literally seeps into the atomic structure of steel pipes, causing “hydrogen embrittlement” that cracks the infrastructure and leaks through standard seals.

Hydrogen carriers

To move hydrogen over long distances, we have to use a carrier molecule—the most practical being Ammonia NH3, one of the most traded substances on earth because it underpins 50% of the global fertilizer market.

There is a second carrier option using specific oils that absorb hydrogen, but the use case remains unproven at the moment.

Turning hydrogen into ammonia relies on the Haber-Bosch process, which mixes hydrogen with nitrogen to make ammonia.

The chemical reaction is

Getting the Nitrogen is easy, air is 78% nitrogen and industrial plants use simple air separation units to suck in air, chill it and separate the nitrogen.

You will hear of Ammonia described as grey, blue and green but that relates entirely to how the hydrogen was produced. The Haber Bosch process is unchanged.

Once the hydrogen is combined into ammonia, it is easy to transport and get to “almost” anywhere. I say “almost” because ammonia is a highly toxic and dangerous chemical that is unlikely to be allowed in city centers without severe permitting restrictions.

Cracking

Once delivered to a site the ammonia goes through a process called Cracking where it is split into Hydrogen and Nitrogen, the nitrogen is released into the atmosphere- back to where it came from and the hydrogen used to fill the tanks of trucks, boats, planes, trains or steel works.

Finally, the hydrogen enters a fuel cell, which uses it to generate electricity.

The Value Chain

That is the complete value chain for the hydrogen ecosystem, and at every stage, there are numerous companies developing innovative solutions; as I have already said, momentum is clearly building. Ballard Power is selling more engines than ever before, validating the downstream arrival of hydrogen, and Plug Power is receiving numerous orders for electrolysis, validating the upstream production of hydrogen.

Is this the time to invest?

It is a difficult question to answer. On one hand, retail momentum is screaming buy as seen by the recent explosive moves in Plug (+45%), Ballard (+72%), and FuelCell Energy (+228%). We are seeing real commercial milestones, like Westport’s heavy-engine initiatives, ITM’s structural moves, and Ballard’s scaling engine sales.

The answer to whether the sector is growing is a nuanced paradox: The physical infrastructure is scaling up significantly, but the corporate playing field is aggressively shrinking.

The Growth Story: Real Hard Assets

If you look at raw capacity, the sector is absolutely expanding. Bloomberg New Energy Finance (BNEF) projections for 2026 show that global clean hydrogen capacity is expanding by approximately 900,000 metric tonnes—a massive 45% year-over-year increase. We are finally moving past non-binding agreements into massive, completed reference assets:

Plug Power has fully installed all ten 10 MW arrays for Galp’s 100 MW green hydrogen facility at the Sines refinery in Portugal, actively replacing 20% of the site’s grey hydrogen.

JSW Energy has successfully commissioned India’s largest 25 MW commercial green hydrogen plant, delivering 3,800 tons of green hydrogen annually directly into a steel mill’s direct reduced iron [DRI] furnace.

Execution Gaps and Corporate Shakeouts

85% of all announced clean hydrogen capacity for 2030 remains stuck in the planning stage. Only 5% has broken ground on actual construction, because a microscopic 2% of announced global supply has locked in an actual buyer.

This lag has triggered a massive, localized industry purge. High costs and rigid rules recently led a group of Spain’s top energy firms to reject €802.85 million in EU subsidies that had been awarded. Giants like Statkraft have completely pulled the plug on their green hydrogen contracts to retreat to core renewables, and developers like Ørsted and Air Products are canceling multi-billion dollar projects. This gridlock has led to bankruptcies among early-stage Western tech providers, including McPhy Energy and Green Hydrogen Systems.

Conclusion: Where is the Alpha

So, is the sector growing? Yes. The physical deployment of hydrogen in heavy industry and steel is structurally inevitable. But the days of picking any generic hydrogen small-caps and winning are over.

Western pure-plays are facing a punishing deflationary price war from Chinese OEMs (like LONGI and Sungrow), who now control over 60% of global electrolyser capacity and undercut Western pricing by 33% to 50%.

To win as investors, we have to look for the lean survivors who are pivoting away from expensive, custom-built construction projects toward standardized, high-margin products.

ITM Power has aggressively cleaned its order book so that 71% of its £152 million backlog is now tied to strictly profitable, standardized contracts.

Nel ASA just launched a next-generation pressurized alkaline platform that slashes capital costs by 40% to 60% while shrinking the physical footprint by 80%.

The “Trough of Disillusionment” is clearing out the weak hands. We need to separate the scalable technology winners from the casualties of the cycle.

In the coming weeks, I will use this framework to detail specific deep-dives into Hydrogen producers, transporters, crackers and fuel cell makers. to see if they possess the balance sheets and product niches to survive the purge and profit on the Slope of Enlightenment.

This final table shows key global assets that have come on line recently and their use cases, if the 45% growth rate of hydrogen production continues this will soon become a substantial profitable business for some.