Robotaxi Market 2030

A $34 Trillion Opportunity

The robotaxi revolution is here, and it is projected to explode into a $34 trillion market by 2030.

This isn't just another tech trend—it's the biggest investment opportunity of the decade.

We're talking about the chance to identify and back the companies that will dominate the future of transportation and deliver massive returns. While technological hurdles and high barriers to entry exist, industry leaders such as Waymo, Baidu, Pony.AI, and others are already operational, while giants like Amazon, Tesla, and Volkswagen are aggressively developing their solutions. The race is on, and the potential rewards are staggering.

The Market Potential

Off the Scale!

$34 TRILLION. That's the equity value Ark Invest forecasts for the robotaxi industry by 2030. Let that sink in. In November 2024, the entire NASDAQ was valued at $30 trillion. This isn't just growth—it's an upheaval.

It represents an opportunity the scale of which is unmatched at present. If these forecasts are even remotely accurate, then the players in this market have a hundred-bagger potential, and Ark is not alone in forecasting extraordinary growth.

Growth drivers

The robotaxi industry is set for significant expansion due to a combination of factors. Technological advancements in self-driving systems, electrification, connectivity, and mapping are making robotaxis safer and more capable. Economically, they promise reduced operating costs, increased efficiency, lower fares, and potentially less need for personal car ownership. Societally and environmentally, robotaxis can alleviate congestion, offer convenient mobility, promote sustainability, enhance accessibility, and improve road safety. Supportive regulatory environments and growing public acceptance, along with strategic partnerships and investments from major industry players, are also crucial drivers of this growth.

The Demanding Nature of Autonomous Driving Development

Developing autonomous driving capabilities is an exceptionally challenging undertaking, requiring the convergence of numerous advanced technologies and engineering fields.

Key Demands:

Sophisticated Perception Systems: Integrating and perfecting sensors (cameras, LiDAR, radar) to accurately interpret complex and ever-changing real-world environments across all conditions.

Intense Data Processing and AI: Handling the massive amounts of sensor data necessitates powerful computing and intricate artificial intelligence and machine learning algorithms.

Robust Decision-Making and Control: Creating reliable systems capable of navigating unpredictable situations, anticipating other road users' behavior, and adhering to traffic laws flawlessly.

Rigorous Testing and Validation: Demanding extensive simulation and real-world testing across diverse scenarios to guarantee safety and reliability.

Even minor errors can have significant consequences. This is a highly regulated, technically difficult endeavor that requires high levels of CAPEX and years of testing.

The Market is Concentrated

The technical difficulty and large CAPEX provide significant barriers to entry, and as a result, there are few players in this market despite its enormous potential.

Six companies have reached commercial operations, and at least five are either currently testing or have announced plans to do so.

The sixth operational robotaxi company is AutoX, a private company operating in two cities in China with a fleet of around 200 taxis. AutoX has multiple agreements with Auto industry players, including Steelantis, to develop its technology and has raised nearly $300 million in 8 funding rounds.

The five companies involved in testing or planning to do so are: Amazon with its Zoox subsidiary, LYFT, Hyundai, Tesla, and Volkswagen.

Company Reviews

The profit potential is immense, but the path to realizing it varies greatly between companies. Investors must prioritize businesses with a clear, realistic roadmap to profitable operations, demonstrating strong execution and financial discipline.

True outsized returns come from identifying those companies positioned for disruptive growth. This means focusing not just on current operational viability, but also on factors like technological superiority, strategic partnerships, and the potential for rapid scalability.

The aim is to find exponential share price growth and deliver truly transformative returns for investors.

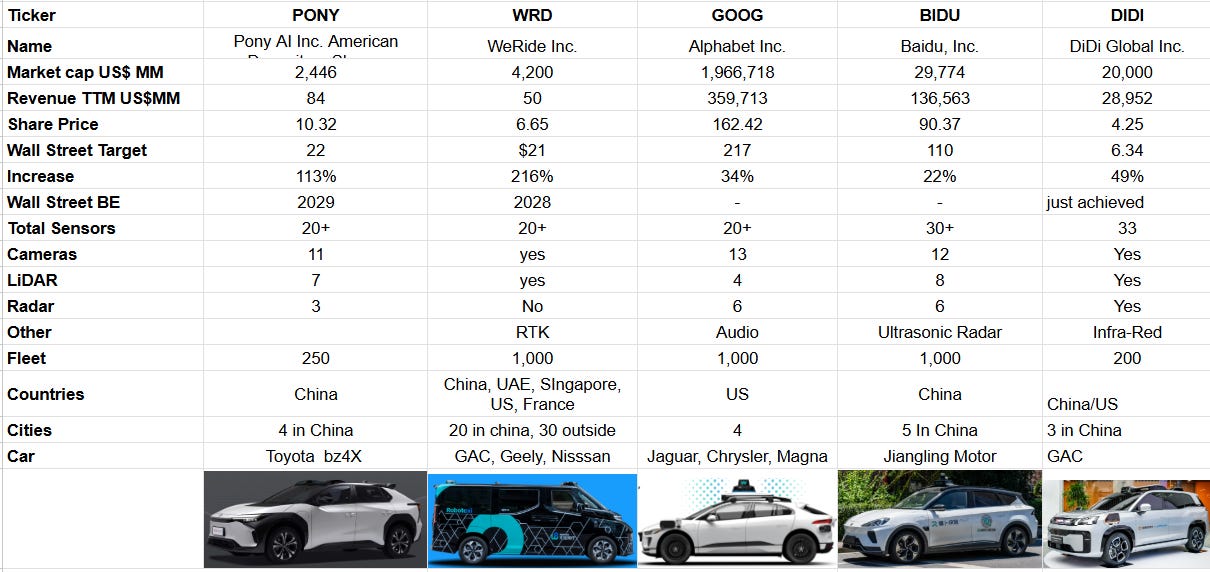

Pony.AI

Pony is in full commercial operation in three cities in China; they are probably in third place in terms of miles covered and taxi rides provided behind Wayom and Baidu. Pony also has a thriving autonomous trucking division that is gaining traction in China and showing growing revenue.

Pony is moving to mass production of its Taxis this year with multiple auto OEM manufacturers.

Strategic Focus: Pony.ai prioritizes "RoboTaxi First," "China First," and "Tier 1 Cities First." They aim to operate a large taxi fleet, integrate with ride-hailing apps, develop their own app, and eventually sell taxis to other operators. They also have a growing autonomous trucking division.

Expansion Plans: The company intends to significantly increase its robotaxi fleet, aiming to scale from 250 taxis to over 2,000 by 2026.

Financial Challenges: Recent financial reports show a decrease in robotaxi service revenue and overall revenue. They face class-action lawsuits and short-selling activities. Despite this, they have a strong cash balance and are focused on growing revenue from taxi fares and freight delivery.

Technological Development: Pony.ai is developing its seventh-generation technology, aiming for reduced manufacturing costs. They use extensive simulations for AI training and have validated their approach with lower insurance costs and successful deployments in complex urban environments.

Regulatory Progress: Pony.ai has secured authorizations to operate robotaxi services in multiple major Chinese cities and is expanding to other regions like Hong Kong, Seoul, and Luxembourg.

WeRide

WeRide is pursuing a diversified autonomous vehicle strategy beyond just robotaxis. They are developing and deploying RoboBuses, RoboSweepers, and RoboVans, believing these vehicles can gain certification more quickly than robotaxis and pave the way for their technology.

WeRide is not currently focussed on being a RoboTaxi operator, this could be a big negative. The disruptive nature of this technology will likely result in the largest profits going to the operators and platform owners.

Diverse Vehicle Types: WeRide offers RoboBuses (deployed in 8 countries), RoboVans (with over 10,000 orders), and RoboSweepers (with multi-million-dollar orders). Total vehicle sales in 2024 were small (91 vehicles) but suggest potential for significant growth.

Business Model: WeRide has a dual business model. Internationally, they sell autonomous vehicles to partners and platforms, offering service and revenue sharing. In China, they operate their own ride-sharing platform, WeRideGo. The Uber partnership in Abu Dhabi is an example of their international strategy.

Technology: WeRide uses a hybrid AI approach, combining an end-to-end model with HD maps and extensive simulated data for rare scenarios. They have accumulated 40 million kilometers of driving data without a safety incident, surpassing some of their competitors.

Financials: WeRide has a strong balance sheet with a three-year cash runway but increasing expenses. Net income is high, but revenue has been flat, and the company is not yet cash flow positive. They anticipate needing to raise significant capital in the near term.

Waymo (GOOG)

Waymo stands as the clear frontrunner in the autonomous driving sector. They boast the largest operational fleet and have executed the most commercial robotaxi rides to date. Waymo is actively providing services in multiple cities across the United States and has recently initiated international expansion with operations in Japan. Notably, Waymo has forged a strategic partnership with Uber in Atlanta and is seamlessly integrated with Google Maps, the world's leading mapping application.

Waymo is an autonomous driving technology company that spun out of Google's self-driving car project in 2016.

Waymo Driver: a sophisticated autonomous driving system that uses a suite of sensors (lidar, cameras, and radar) and artificial intelligence (AI). The system uses both real-world driving (tens of millions of miles) and simulation (tens of billions of miles).

Ride-hailing service: Waymo operates a commercial robotaxi service called "Waymo One" in several cities, including Phoenix, San Francisco, Los Angeles, and Austin. In Austin, the service is also available through a partnership with Uber.

Proven Operations: Their data indicates a significant reduction in crash rates compared to human drivers in the areas where they operate.

Expansion: Waymo is actively working to expand its service to new cities, with plans for Atlanta and Tokyo. They are also exploring applying their autonomous technology to personally owned vehicles through a partnership with Toyota.

Mapping: Before operating in a new area, Waymo creates highly detailed custom maps that their vehicles use in conjunction with real-time sensor data for precise localization.

Baidu

Baidu is often called the Google of China; it is the dominant search engine in China. Their robotaxi offering is called ApolloGo, and they enjoy a similar leadership position in China as Waymo does in the US. Baidu has driven more miles than Waymo but has a similarly sized fleet, perhaps benefiting from the dense Chinese cities it operates in.

Baidu's Apollo Go robotaxi service experienced a 36% year-over-year increase in rides in Q4 and anticipates even higher growth in 2025. Baidu considers its sixth-generation robotaxi, the RT6, to be the most cost-effective globally and boasts that its autonomous driving technology is world-leading. Additionally, Baidu is expanding its operations into Hong Kong, a right-hand drive market, coinciding with Waymo's expansion into Japan, also a right-hand drive market. This move into right-hand drive territories is seen as valuable for testing and refining their virtual drivers. While these markets are not the largest, they include significant, dense cities like Tokyo, London, and Kuala Lumpur, making them an important segment of the robotaxi market.

Didi Global

Baidu might be the Google of China, but DiDi is the Uber of China. They bought UBER China in 2016 and became the dominant player in the Chinese ride-hailing market with a 90% market share. Following regulatory scrutiny following its US IPO, DiDi’s market share has fallen to less than 70%, and it was forced to delist from the NYSE by Chinese regulators. DiDi has become a major player in both Latin America and the Asia Pacific region, and has formed a new division for robotaxis.

DiDi Global's robotaxi division, DiDi Autonomous Driving, has been making significant strides in the development and commercialization of its Level 4 autonomous driving.

GAC Aion Partnership: focused on autonomous electric robotaxis.

Mass Production Target: The end of 2025, a crossover SUV built on GAC Aion's AEP 3.0 electric platform and incorporates DiDi's autonomous driving hardware and software.

Technology: featuring 33 sensors including lidar, cameras, 4D millimeter-wave radar, infrared cameras, and sound sensors for 360-degree perception.

Huiju Port System: to manage the robotaxi fleet, enabling functions like automated ride acceptance, charging, maintenance, and parking. The robotaxis will be integrated into DiDi's existing ride-hailing network using a mixed-dispatch model alongside human-driven vehicles.

The company is strategically focusing on the Chinese market, aiming for large-scale deployment and integration of robotaxis into its existing ride-hailing platform. While challenges in regulation, technology scaling, and competition remain in the broader autonomous vehicle industry, DiDi's progress in securing manufacturing capabilities and advancing its technology positions it as a key player in the evolving robotaxi landscape. The target of mass production by the end of 2025 is ambitious and will be a critical milestone to watch.

Future Entrants

There are five players with plans to enter this market. Here is a review of their status.

Amazon

Amazon bought its Zoox robotaxi subsidiary in 2020 for $1.2 billion. Zoox operates as a stand-alone unit and has some unique attributes compared to the competition.

Technology and Vehicle:

Purpose-Built Robotaxi: Zoox distinguishes itself by developing a fully autonomous, all-electric vehicle from the ground up, designed explicitly for ride-hailing. This vehicle has no steering wheel or pedals and can travel up to 75 mph.

AI and Software: Zoox develops its proprietary AI and software in-house, enabling the vehicles to perceive, predict, plan, and control their movement in complex urban environments.

Safety Focus: More than 100 safety innovations have been integrated into the vehicle, including a unique horseshoe-shaped airbag system. Zoox was the first to self-certify a purpose-built, fully autonomous, electric.

Testing in Multiple Cities: Zoox is actively testing its robotaxis in several key locations: Las Vegas, Nevada: Expected to be their first commercial market.San Francisco, Foster City, California (Headquarters): Austin, Texas and Miami, Florida: Mapping missions have begun in these cities, with plans to deploy test fleets with safety drivers eventually.

They also had an expanded partnership with Uber to bring their robotaxi services to Austin and Atlanta.

Hyundai

Motional, an autonomous vehicle company formed as a joint venture between Hyundai Motor Group and Aptiv, intends to begin ride-hailing operations in 2026. Hyundai has increased its ownership of Motional as Aptiv has entered a period of restructuring. Aptiv provides the sensor pack and much of the autonomous hardware and software for the venture.

Partnerships: Motional has strategic alliances with Lyft for autonomous ride-hailing and Uber Eats for autonomous delivery services.

Technology Focus: Motional utilizes an Aptiv-based system, with a particular emphasis on radar technology, for its autonomous driving platform.

Testing and Development: Motional is actively expanding its testing operations in urban centers like Pittsburgh and Las Vegas, increasing its operational domain and exposing its technology to complex driving scenarios.

Milestones: The company has recently achieved a significant milestone by initiating highway speed driving and testing.

Electric Vehicle Platform: Motional deploys its autonomous driving technology on the all-electric Hyundai IONIQ 5 robotaxis.

Joint Venture Evolution: The joint venture structure has evolved, with Hyundai increasing its investment and commitment, positioning Motional as a leader in autonomous mobility on-demand solutions.

LYFT

The second major ride-hailing platform in the US has about a 24% market share compared to Uber’s 74%. LYFT primarily pirates in North America revenue is around $1 billion a tenth of UBER’s. LYFT has indicated it will begin operating robotaxis soon and has already clocked more than 100,000 “ride-hailing experiences” using technology supplied by APTIV under an agreement that started in 2018.

Hybrid Network Approach: Lyft envisions a future where autonomous vehicles (AVs) and human drivers work together. They believe this "hybrid network" will provide the most efficient and reliable transportation system.

Partnerships: Lyft is collaborating with several companies to advance its AV initiatives. These include partnerships with:

May Mobility: To deploy autonomous Toyota Sienna minivans on the Lyft platform, starting in cities like Atlanta.

Mobileye: To integrate vehicles equipped with Mobileye's autonomous driving technology into the Lyft network.

Deployment Plans: Lyft has announced plans to begin offering autonomous rides to its customers as early as this summer in 2025.

Tesla

Tesla makes the most noise about robotaxis and its big supporters, like Ark Invest, fervently believe that Tesla will dominate the robotaxi market, turning it into the world's largest and most profitable company. In Q1 earnings, the CEO said Tesla will begin with 10 Robotaxis and scale to millions by the end of 2026, users will use a yet-to-be-released Tesla app, and owners of Tesla cars will rent out their vehicles to provide the service.

Tesla will hold a robotaxi day in June, where we should get detailed information; however, I am very skeptical about Tesla.

Every other company working in this field is adamant that for safe operations, a full sensor suite including LiDAR, long-range Radar, Cameras, plus Ultrasound and short-range radar is required. The other companies all perform detailed mapping operations before starting operations. Tesla may have achieved this through its vehicles in the field, but it is unclear.

Tesla have so far said they can do this with their camera only FSD software, there is ample reason to be cautious with this claim. In the US, the NHTSA is investigating several incidents where FSD may have malfunctioned under challenging visibility conditions. In China, Tesla had to seek help from Baidu for its FSD v13, which appears unable to drive safely on Chinese roads.

Volkswagen

Volkswagen Group is making significant strides in the development and deployment of autonomous driving technology, with a clear focus on both Europe and the United States.

MOIA and Robotaxi Ambitions

MOIA: a subsidiary of the Volkswagen Group, is playing a crucial role in the company's autonomous driving strategy. MOIA is focused on developing on-demand ride-pooling services.

ID. Buzz AD: Volkswagen Commercial Vehicles is developing the ID. Buzz AD, an autonomous version of the electric ID. Buzz van, specifically for use in these ride-pooling services.

Testing and Deployment: MOIA has been testing the ID. Buzz AD in various cities, including Hamburg, Munich, Oslo, and Austin, Texas.

Hamburg Focus: MOIA aims to launch an integrated autonomous ride-pooling system in Hamburg, with plans for international scaling. They are working towards deploying autonomous vehicles in Hamburg's city center by 2025.

Testing: MOIA has begun testing with select customer groups.

United States: Volkswagen is also making a significant push in the U.S. market.

Volkswagen Group of America's subsidiary, Volkswagen ADMT, LLC, is leading the autonomous driving vehicle program in the U.S.

Partnership with Uber: Volkswagen and Uber have announced a strategic partnership to deploy fleets of autonomous ID. Buzz AD vehicles on the Uber platform in multiple U.S. cities over the next decade, starting with Los Angeles.

Testing is set to begin in Los Angeles, with plans to offer rides on the Uber platform in 2026.

Volkswagen is also testing its autonomous vehicle technology in Austin, Texas.

Mobileye: Volkswagen is collaborating with Mobileye autonomous driving technology.

Mobileye is providing technologies for partially and highly automated driving based on its Mobileye SuperVision and Mobileye Chauffeur platforms.

Mobileye is also supplying software and hardware components for the self-driving ID. Buzz AD.

Argo AI: Volkswagen (and Ford) previously partnered with Argo AI.

CARIAD: Within the Volkswagen Group, is developing autonomous software.

China: In China, Volkswagen is collaborating with Horizon Robotics

Conclusion and Next Steps

The robotaxi industry presents an extraordinary investment opportunity, projected to reach a $34 trillion market by 2030. The significant technical challenges and capital requirements create high barriers to entry, concentrating the market among a select few companies with immense profit potential. As I continue my research, I will meticulously analyze each company's technological advancements, market strategies, and financial stability before making investment decisions. My goal is to capitalize on this transformative technology and achieve substantial returns. I will closely monitor this rapidly evolving industry in the coming years to identify and capitalize on the most lucrative opportunities.

Great stuff. Do you see China investing in companies such as PONY? It seems to me that they want to be ahead of other countries. That can be a positive for shareholders.

Google FTW?