Byrna Technologies: Raising My Revenue Target & Increasing My Position

Company Update

Introduction

If you are unfamiliar with Byrna Technologies (BYRN), it is a US company that designs and manufactures less lethal handguns. The devices look like traditional handguns but are C02-powered launchers that send plastic projectiles containing irritants at sufficient speed to stop an assailant at 60 feet.

This is an image of their best-selling device. The Byrna SD

Byrna uses an influencer marketing strategy that has driven an incredible rate of revenue growth since its inception in 2023. The company recently signed a deal to open Byrna Stores inside Sportsman Warehouse sites and has developed 4 retail facilities. The majority of sales are made on Amazon and via its own Website.

The company has been campaigning hard to increase the acceptance of its products, with the CEO doing many interviews in the last 12 months. His main goal is to enable the company to advertise its products on mainstream and social media, something they have been banned from doing since mid-2023.

Q1 Earnings News

Byrna Technologies reported a 50% year-over-year revenue increase to $26.2 million in Q1 2025; traditionally, Q1 is their slowest quarter. This Q1 performance was only 6% below Q4 2024, the drop is usually 47%. Amazon sales have surged, representing 32.6% of Direct-to-Consumer (DTC) sales. Byrna has appointed an Amazon business manager to capitalize on this channel further. Advertising Return on Ad Spend (ROAS) on Amazon was notably high at 18.5 times, compared to 4.5 times on Byrna.com.

Sportsman's is expanding its partnership with Byrna, including 13 "store within a store" locations and adding Byrna shooting lanes in 41 stores, totaling 54 locations where customers can experience the product. The Sportsman’s deal is an important part of the future growth for Byrna; the first store has just opened, and the rest will open next month. Byrna is placing trained representatives in partner stores, aiming for one to five Byrna sales per day per location, translating to almost $ 1 million in annual revenue per store.

To mitigate tariffs, Byrna has increased US content in their launchers to 92%, adding 14% to the cost of a launcher. The new Compact Launcher (CL) is launching soon, priced at $549.99, which is $170 more than the Byrna SD ($379.99) and $70 more than the Byrna LE ($479.99). The CL is 38% smaller and 36% lighter than the Byrna SD, yet equally powerful. It's also 27% narrower, making it ideal for concealed carry and appealing to the women's market. The CL uses a proprietary .61 caliber round, initially available exclusively from Byrna.

Byrna has 11K CL units in stock and is producing 1,000 per day, aiming for over 25,000 units before release. Sample launchers will be sent to partners, endorsers, and stores. The Fort Wayne factory can adjust production between CL, SD, and LE models based on demand. The CL will initially be available in orange and black, with pink and other colors, including customizable options, to follow. Accessories will also be rolled out later this year.

As I noted in my February article, the new launcher follows a well-established pattern in the handgun industry, which has led to an enormous increase in sales.

Impact

Byrna beat on top and bottom lines as they did throughout 2024. The 50% increase YoY sales was above my forecast of 40%, suggesting I have underestimated the company's growth path. The new CL launcher will be critical. Byrna management clearly believes this product will be a home run and is suggesting a huge volume of sales.

In February, I presented my mathematical model, which forecasts a share price of $86, more than 300% above today's figure. The key driver of the forecast is revenue growth, and my assumptions are shown below.

DTC sales increased $7 million in the Quarter. Management guided to quarter-on-quarter growth throughout 2025. I am upgrading this vertical to $102 million, 16% higher.

The revenue of Owned Shops and Dealers increased 78%. Chain store revenue is growing quickly Bass Pro took $700k in product in the quarter. Byrna will have all four of its retail stores open for the rest of the year, probably generating an additional $1.5 million. I need to increase the revenue target for Owned Shops and dealers to $35 million, 40% higher.

Store-in-Store revenue at Sportsmans is likely to be lower than forecast.

The Byrna-owned stores are doing less volume than I had anticipated, an average of $1,350 per day. Their volume is limited by footfall, but they have a high conversion rate. Sportsmen have a much higher footfall with hundreds of visitors each day, however, not many of them will be looking for a Byrna, so conversion will be much smaller. Until we have more information, I am going to assume the owned shops and store-in-store shops get the same revenue, and the 41 POS/shooting lane stores do 25% of that amount. That gives a revised target for SportSmans of $8.5 million, a reduction of 30% from my initial forecast.

My revised Revenue Target is $145 million for 2025. That is a significant increase of 17%.

Decisions

We are long Byrna, the entry prices are shown in this chart.

The combined position shows a profit of 23%, but is very close to the maximum I allow. Position size is very important when trading these smaller companies. At the moment, the maximum investment allowed on the demonstration portfolio is $500, and as a result, I will add 5 additional shares when the markets open on Monday.

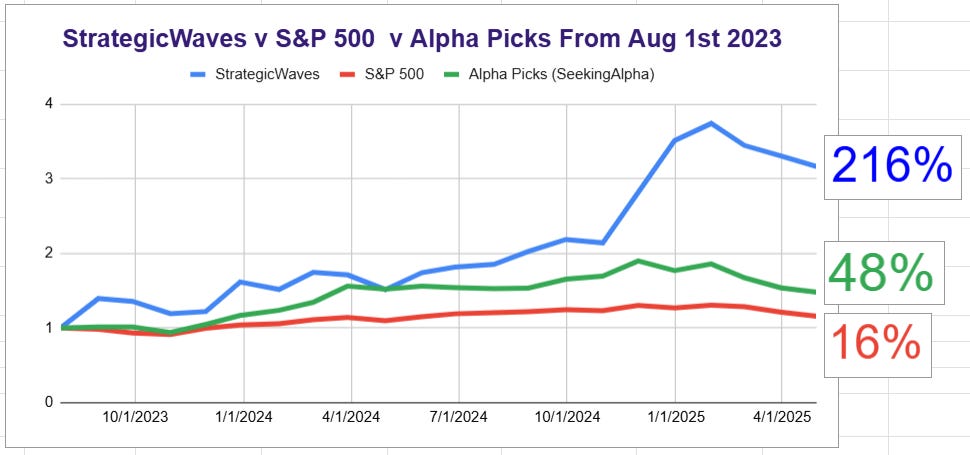

If you are not familiar with the demonstration portfolio, it is one I use to showcase my trading. I invest $250 each month on IBKR US and have been trading it since August 2023. So far, it has shown more than 200% return and has more cash in the account than I invested, as well as more than $5,000 in stocks.

Other News

The SES investment last week looks quite well timed but it was very small, I will look to increase that position next week buying an additional 200 shares.

As you may remember, I was keen to buy Xiaomi last week, but was delayed with tariff concerns. It would have been better to buy. Hindsight is a great thing. If we see another pullback, I will buy

Last week Fox News reported that the Trump administration is considering de-listing Chinese stocks from the US exchanges. I hope that will not happen but it will cause increased volatility that we may be able to take advantage of. If De-Listing looks like becoming a reality I will exit the ADS shares and buy them on another exchange.

Portfolio Performance

The portfolio continues to outperform the markets but is down this month. My base case prediction is now for a significant upturn in the second half of the year. I expect to see the US return to growth and a flurry of trade deals to be signed, some with the US and some with China, but they will all lead to growth. I hope to invest most of our large cash balance in Q2 to take advantage of growth later in the year.

Newsletter

I will turn on the paid newsletter's first stage on May 1st. Thanks to the people who have pledged in advance, it will pay for a significant upgrade to my IT and enable me to increase the financial subscriptions I have. It will mean better research, faster turnaround times, and hopefully more profit from trading.

I haven't yet raised enough to buy the institutional-quality platform I aim for, but hopefully, we will get there this year.

Stephen, where do I go to contribute to your launch of your upcoming private service?