AI Bubble? A Looming Write-Down for the Ages

The chips are becoming obsolete to quickly for these investments to make sense.

I recently covered OWL 0.00%↑ in a weekly review, noting its “Iron Clad” contracts, giving it some immunity from the private credit problems surrounding AI infrastructure.

In this article, I expand my thoughts looking at recent deal collapses and honing in on the “chip” problem that may develop into a serious problem for the hyperscalers. They will still be on the hook to Owl, but they may not be able to use the facilities as expected.

Greed and History

The markets are currently gripped by what I can only describe as “Giga-Watt Glamour.” From the boardrooms of Menlo Park to the sovereign wealth funds of the Gulf, the consensus remains that more is more: more chips, more data centers, and more debt. But as an analyst who lived through the fiber-optic glut of 2001, the current trajectory of AI infrastructure doesn’t look like a revolution; it looks like a stranded asset crisis in the making.

The Crumbling Pillars of the “Mega-Deal”

For the past year, we’ve been fed a diet of trillion-dollar headline figures. Yet, when you look past the press releases, the structural integrity of these deals is failing.

Take the Oracle-OpenAI-Nvidia nexus. Just last week, reports confirmed that OpenAI walked away from a flagship expansion in Abilene, Texas—part of the much-vaunted “Stargate” initiative. The reason? OpenAI reportedly realized the facility would be obsolete before the concrete even dried. They wanted Nvidia’s newer Rubin architecture, not the Blackwell chips Oracle had already leveraged its balance sheet to procure.

This isn’t an isolated “pivot.” It’s a fundamental breakdown in the “build it and they will come” philosophy. In the UK, the “Stargate UK” project, once touted as the cornerstone of a “sovereign AI superpower,” has effectively stalled. Domestic power constraints and a sudden chilling of government subsidies have left several planned sites in the North East looking more like speculative real estate than the future of intelligence.

Meta: The Canary in the GPU Mine

While Microsoft and Google continue to spend as if capital is free, Meta has begun to blink. Despite Zuckerberg’s public bravado about “personal superintelligence,” the internal reality is grim. Meta is currently preparing to slash its workforce by upwards of 20%—a desperate move to offset the staggering $135 billion in capital expenditure projected for 2026.

When a company begins firing the very engineers needed to build the software because the “hardware tax” is too high, you are witnessing a business model in conflict with its own balance sheet. Meta’s abandonment of its “Behemoth” model last summer was the first sign that even the deep-pocketed hyperscalers are hitting a wall of diminishing returns.

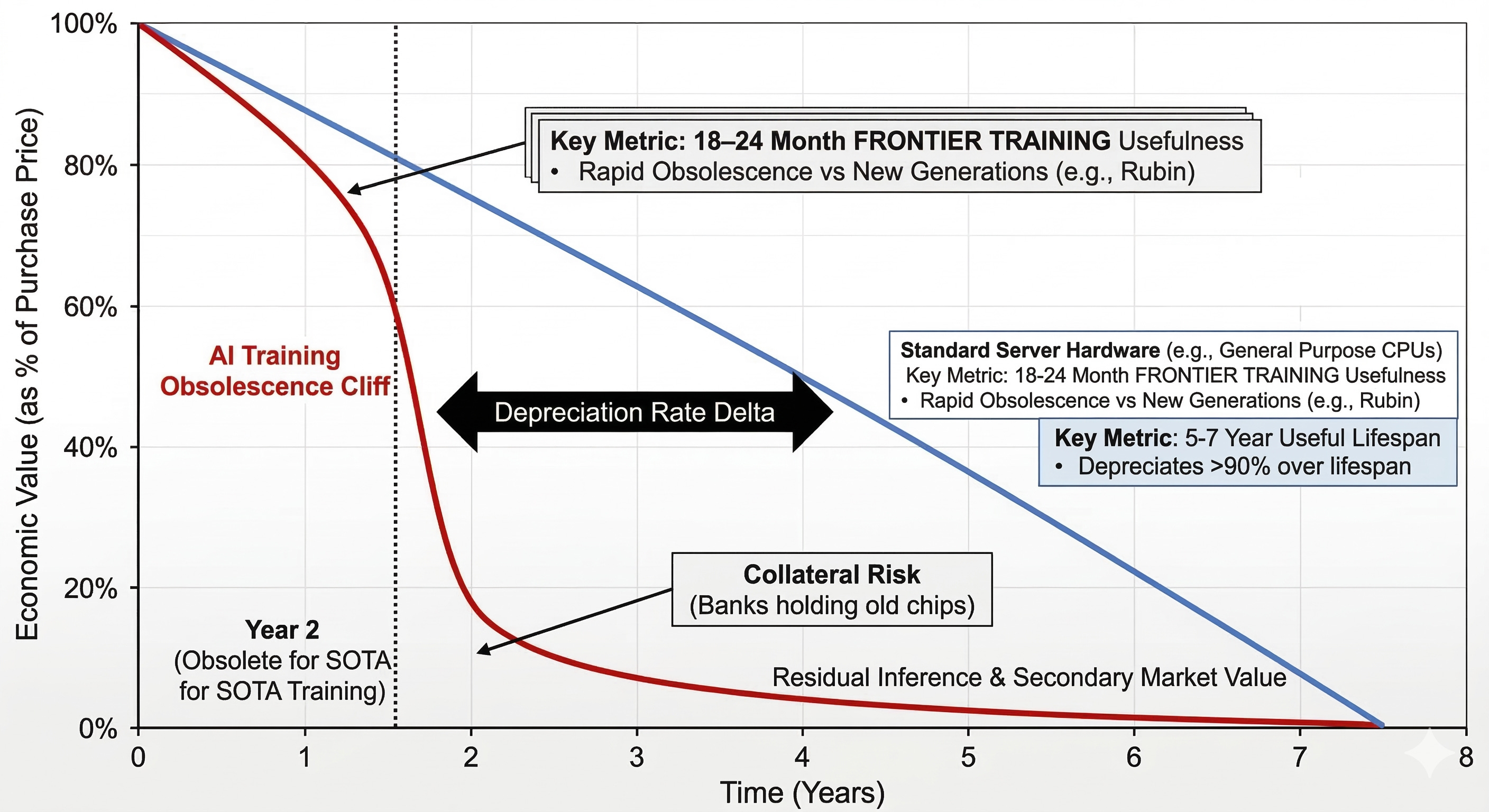

The Terminal Velocity of Depreciation

The most overlooked risk in this entire cycle is the economic half-life of a GPU. In traditional infrastructure, a gas turbine or a server rack is depreciated over five to seven years. In the AI arms race, the “useful life” of a chip for frontier training is now roughly 18 to 24 months.

When a new architecture (like Rubin) arrives, the previous generation (Blackwell or H100) doesn’t just become “slower”—it becomes economically unviable for the highest-value workloads.

The Power Trap: Newer chips offer more “tokens per watt.” As energy becomes the scarcest resource, running “old” silicon is essentially burning money.

The Collateral Crisis: This is where the banks get burned. Many of the “Compute SPVs” (Special Purpose Vehicles) used to fund these data centers use the GPUs themselves as collateral.

Note: If a bank holds $10 billion in Blackwell chips as collateral, and a sudden architectural leap renders those chips 50% less efficient than the new standard, the “value” of that collateral evaporates overnight. We are looking at a potential wave of under-collateralized loans that could freeze private credit markets faster than you can say “margin call.”

The Verdict: A Desert of Empty AI Facilities

We are currently seeing a record number of data center cancellations—26 in the last quarter alone by some counts. Between grassroots opposition, grid instability, and the realization that the revenue from AI “agents” isn’t yet covering the interest on the debt, the “Mega-Deal” era is ending.

The winners of the next three years won’t be the companies with the most H100s in the ground; they will be the ones who didn’t sign the 10-year lease on a facility designed for yesterday’s technology. For the rest? Expect a decade of painful write-downs.

Could you write a disclaimer when you write articles with Ai?? I pay quite a lot of money for this service each year as I would much rather read your writing than Ai writing

And if you were to short those that would be hit by this, who would you choose?